Rental Property Tax Guide for Landlords (2026 Edition)

Rental property taxes don't have to be a once-a-year panic. A simple monthly habit makes April a 30-minute job instead of a weekend.

Disclaimer: This guide is general information for landlords, not personalized tax advice. Tax law is complex and changes year to year. Talk to a CPA who works with rental property owners before filing.

The frustrating thing about rental property taxes is that 80% of the work happens during the year, but most landlords don't realize that until April. By then, half the deductions are missed because nobody saved the receipts, the mileage log doesn't exist, and the line between "repair" and "improvement" is a guess.

This guide is the year-round version. What to track, what to deduct, what to depreciate, and what to do every month so April is a 30-minute job.

How is rental income taxed in the United States?

Rental income is taxed as ordinary income at your regular federal tax bracket. It's reported on Schedule E of IRS Form 1040, and the net rental income (after deductions) flows through to your personal return.

The good news for most landlords:

- Rental income is passive income, not earned income, so it's generally not subject to self-employment tax (the 15.3% you'd pay if you were a freelancer).

- You can deduct a long list of expenses against rental income.

- You can also deduct depreciation, which is a non-cash expense that often produces a paper "loss" even when the property is cash-flow positive.

The bad news:

- The IRS expects detailed records. "I think I spent about $4,000 on repairs" is not a deduction. A receipt for $4,237.84 is.

- Passive losses are limited. If your rental shows a loss, you generally can't deduct more than $25,000 of it against other income (and that phases out as your income rises). Excess losses carry forward, but they don't disappear.

- Improvements vs. repairs is the line landlords get wrong most often, and it's the line the IRS audits most aggressively.

What rental property expenses can I deduct?

Here are the categories that go on Schedule E. If you spent money on it during the year and it's tied to the rental, it almost certainly fits in one of these.

| Category | What it covers |

|---|---|

| Advertising | Listing fees, photographer for unit photos, signs |

| Auto and travel | Mileage to the property for management purposes |

| Cleaning and maintenance | Recurring cleaning, pest control, lawn care |

| Commissions | Real estate or leasing commissions |

| Insurance | Landlord/dwelling insurance, umbrella policy (rental portion) |

| Legal and professional fees | CPA, attorney, eviction filing fees |

| Management fees | Property management company fees |

| Mortgage interest | Interest only — principal is not deductible |

| Repairs | Fix-it work that maintains existing condition |

| Supplies | Paint, lightbulbs, batteries, filters |

| Taxes | Property tax (state and local) |

| Utilities | Any utilities you (not the tenant) pay |

| Depreciation | Annual deduction for the building's wear and tear |

| Other | HOA fees, license fees, banking fees on the rental account |

A few specific items landlords often miss:

- Mileage to and from the property for inspections, repairs, showings, tenant meetings. Track date, miles, and purpose. The IRS standard mileage rate updates annually.

- Software and tools you use for landlording — including the cost of property management software like PropertyLens, accounting tools, screening services.

- Bank fees on a dedicated rental account.

- Continuing education like landlord conferences, books, or courses (within reason).

- Home office if you have a dedicated space used regularly and exclusively for managing rentals.

What's the difference between a repair and an improvement?

This is the single most expensive distinction in rental tax law to get wrong. The IRS treats them very differently:

- Repairs maintain the existing condition of the property. They are fully deductible in the year you incur them.

- Improvements add value, extend the useful life, or adapt the property to a new use. They must be capitalized and depreciated over multiple years (usually 27.5 for residential).

Here's how the line typically gets drawn:

| Repair (deduct in year) | Improvement (depreciate over years) |

|---|---|

| Patch a hole in drywall | Knock out a wall to enlarge a room |

| Replace a broken window | Replace all windows with energy-efficient upgrades |

| Fix a leaky faucet | Replace the entire plumbing system |

| Repaint a room | Whole-house exterior repaint after siding replacement |

| Service the HVAC unit | Install a new HVAC system |

| Replace a few damaged shingles | Install a new roof |

| Refinish hardwood floors | Install new hardwood floors |

| Replace a broken appliance | Renovate the entire kitchen |

Why does this matter? A $15,000 kitchen renovation deducted as a repair gets you a $15,000 deduction this year. The same renovation correctly classified as an improvement gets you about $545/year for 27.5 years. The first version is wrong, and an audit will catch it.

The De Minimis Safe Harbor is the landlord-friendly exception: items costing $2,500 or less per invoice can be expensed in the year of purchase even if they would technically be improvements. Make sure to attach the election statement to your return.

How does depreciation work on a rental property?

Depreciation is the IRS letting you deduct a slice of the building's cost every year, even though you didn't actually spend cash on it that year. It's the most under-utilized deduction in the small-landlord world.

The math, simplified:

- Take your purchase price (or basis) for the property.

- Subtract the value of the land — land doesn't depreciate. If you don't have an appraisal that splits land vs. building, the property tax assessment usually shows the breakdown.

- The remainder is your depreciable basis.

- Divide by 27.5 (for residential rentals; it's 39 for commercial) to get your annual depreciation deduction.

Example:

- Purchase price: $300,000

- Land value (per tax assessment): $60,000

- Depreciable basis: $240,000

- Annual depreciation: $240,000 ÷ 27.5 = $8,727 per year

That $8,727 is a deduction against your rental income every year for the next 27.5 years, without you spending a dime. For many small landlords this is what turns a cash-positive rental into a paper-loss rental for tax purposes — which is good, because the loss can offset other rental income or carry forward.

Watch out for depreciation recapture. When you eventually sell the property, the IRS recaptures the depreciation you took (at a max 25% rate). It's not a free deduction — it's a deferral. Most CPAs still recommend taking it because the cash-flow benefit now outweighs the recapture later, but talk to yours before assuming.

What records do I need to keep for rental property taxes?

Keep records for at least 7 years to cover the IRS audit window. Specifically:

- Receipts and invoices for every expense, with date, amount, vendor, and what it was for.

- Bank and credit card statements for the rental account (and the personal accounts if you mixed funds — though don't mix funds).

- Mileage logs with date, miles, and business purpose.

- Lease agreements and tenant ledgers.

- Closing documents from the property purchase. You'll need these forever — they establish your basis for depreciation and capital gains.

- Major repair / improvement invoices, kept separately and indexed. Improvements get added to your basis at sale.

- Insurance and property tax statements.

- 1099s and W-9s for any contractor you paid more than $600 in a year (you have to issue these).

The single best habit: scan or photograph every receipt the day you get it, attached to the property and category it belongs to. Software like PropertyLens lets you snap a photo and tag it on the spot. The receipt sitting in the truck cabin in July is a deduction you'll forget by April.

What are the most common landlord tax mistakes?

After watching landlords go through their first audit, the same five mistakes show up over and over:

- Treating improvements as repairs. The big-ticket one. Easy to fix if you slow down before deducting any work over $2,500.

- Forgetting depreciation entirely. A surprising number of self-filing landlords don't take depreciation because they don't know about it. You can amend prior returns (3 years back) or use Form 3115 to claim missed depreciation.

- Mixing personal and rental finances. A single personal-and-rental bank account turns every audit into a forensic accounting exercise. Open a dedicated bank account and credit card for the rental.

- No mileage log. "I drove there a few times" doesn't deduct. A contemporaneous log of date / miles / purpose does.

- Ignoring the passive activity loss rules. Reporting a $40,000 rental loss against your $80,000 W-2 income is going to get questioned. The cap is $25,000, phased out above $100,000 MAGI, with full phase-out at $150,000 (unless you qualify as a real estate professional).

How do you make tax season easy?

The system that works:

- Open a dedicated rental bank account and credit card. Run every rental dollar through these. No exceptions.

- Categorize every expense as it happens — repairs, supplies, utilities, etc. Software does this automatically; spreadsheet users tag manually.

- Photograph receipts on the spot. Most receipts are unreadable thermal paper after six months in a glove compartment.

- Keep a mileage log in real time. A free phone app (or PropertyLens's built-in tracker) is fine.

- Reconcile monthly. Match the bank statement to your ledger. Fix discrepancies before they compound.

- Run a quarterly summary. Make sure the categories look right and the numbers are sane.

- In April, hand your CPA a clean export. Don't make them reconstruct your year.

A landlord who follows this system spends about 15 minutes a month on taxes and 30 minutes in April. A landlord who doesn't spends a weekend in April rebuilding the year and another weekend after the audit notice.

What's a Schedule E and how do I fill it out?

Schedule E (specifically Part I for rental real estate) is the IRS form where rental income lives. It's not as scary as it looks.

For each property, you report:

- Address and type of property

- Number of fair rental days (days rented at market rate) and personal use days

- Income: total rents received

- Expenses by category — the categories listed in the table above each get their own line

- Depreciation

- Total expenses subtracted from income to give net rental income or loss

Most tax software (TurboTax, H&R Block, FreeTaxUSA) walks you through Schedule E line by line. If you have more than 2–3 properties or any complexity (1031 exchange, partnership, refinancing), use a CPA who specializes in real estate. The fee is itself a deduction.

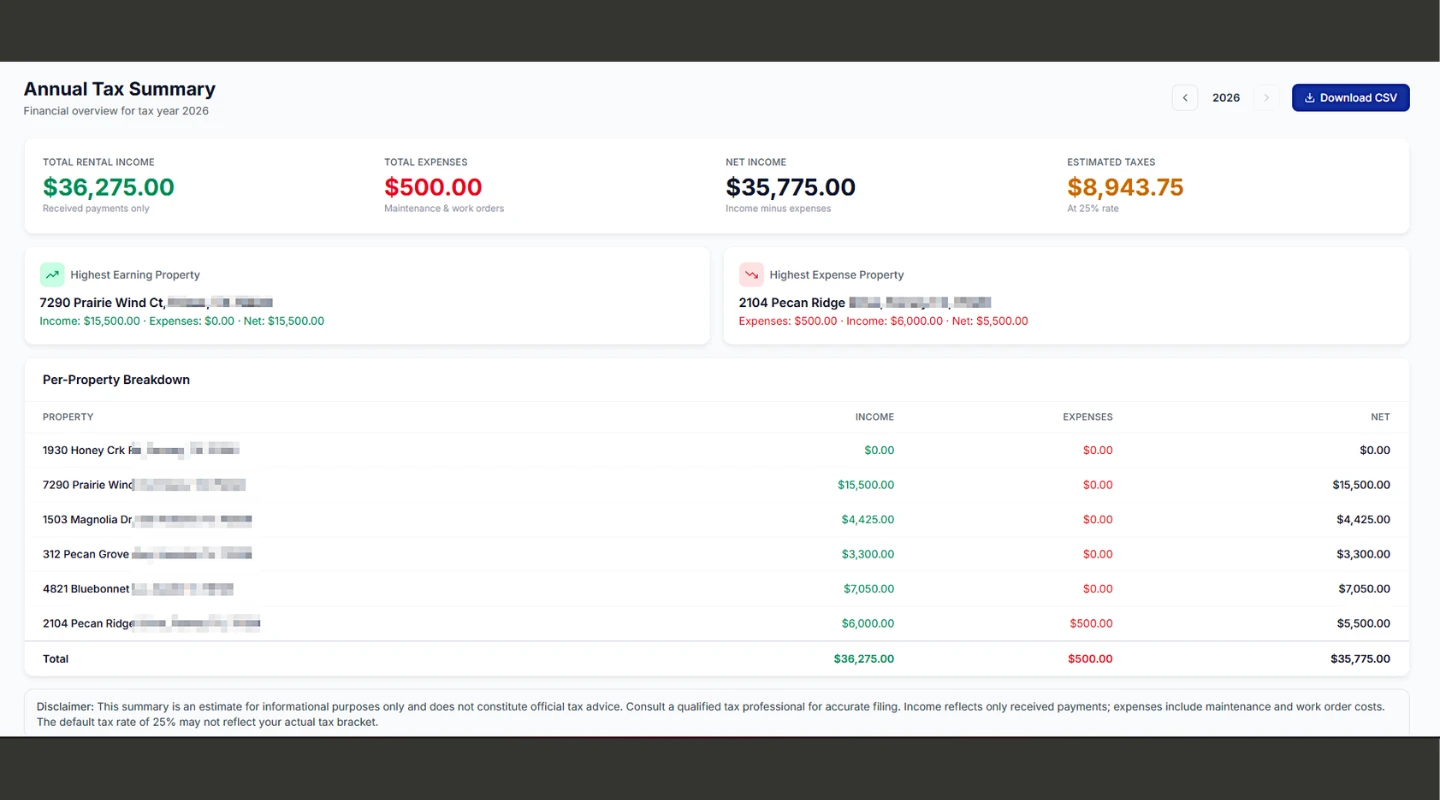

PropertyLens generates a Schedule E–ready summary by property, by category, with depreciation pre-calculated, that you can hand directly to a CPA or paste into tax software. Try it free →

Ready to stop juggling spreadsheets?

PropertyLens tracks rent, manages tenants, and handles maintenance — free for your first property.

Start freeFrequently asked questions

What rental expenses are tax-deductible?

Common deductible expenses include: mortgage interest, property tax, insurance, property management fees, repairs and maintenance, advertising for tenants, utilities you pay, professional fees (CPA, attorney), HOA fees, travel to the property for management purposes, supplies, and depreciation of the building.

What's the difference between a repair and an improvement?

Repairs maintain existing condition (fixing a leaky faucet, replacing a broken window) and are fully deductible in the year you incur them. Improvements add value or extend useful life (new roof, kitchen renovation, addition) and must be depreciated over multiple years. Mixing these up is one of the most common audit triggers.

How do I depreciate a rental property?

Residential rental property is depreciated over 27.5 years using straight-line depreciation on the building's value (not the land). If you bought a property for $300,000 and the land is worth $60,000, you depreciate $240,000 over 27.5 years — roughly $8,727 per year as a deduction.

Do I have to pay self-employment tax on rental income?

Generally no. Rental income is considered passive income for most landlords and is not subject to the 15.3% self-employment tax. Exceptions: if you provide substantial services to tenants (cleaning, meals, like a B&B) or if you're a real estate professional under IRS rules, the treatment changes.

Can I deduct travel to my rental property?

Yes, if the trip's primary purpose is property management — inspections, repairs, showings, tenant meetings. You can deduct mileage at the IRS rate or actual costs (gas, parking, tolls). Keep a contemporaneous log of date, miles, and purpose. Travel that combines management with personal time gets prorated.

What's a Schedule E and how do I fill it out?

Schedule E (Form 1040) reports rental income and expenses to the IRS. You list each property separately, report gross rents, then itemize deductible expenses by category (advertising, insurance, repairs, etc.). The bottom line is your net rental income or loss. Most rental income flows through to your personal 1040 from here.